Earnings do the heavy lifting

Key takeaways

- Earnings are in the driver’s seat. Strong and accelerating corporate profits are offsetting headwinds from higher energy prices, inflation pressures, and central bank uncertainty.

- Economic fundamentals remain solid. Canada GDP growth looks to have rebounded in the first quarter as did U.S. GDP. Business investment is surging, and consumers continue to spend, suggesting the North American economy is holding up for now despite rising costs.

- AI remains a key profit engine. Accelerating investment in AI and related infrastructure continues to help support earnings growth across technology and other sectors.

- After a strong rally, risks appear more balanced. We may see more market volatility ahead, but as long as corporate earnings remain solid, investors have reason to stay constructive and tune out short‑term headline noise, in our view.

April capped a sharp V‑shaped recovery, with the TSX gaining 3.6% and the S&P 500 rising 10%, its strongest monthly gain since November 2020. This advance came despite ongoing geopolitical uncertainty and lingering energy concerns. That apparent disconnect has left many investors asking a familiar question: why are markets holding up so well?

In our view, the answer is corporate earnings.

Markets today are navigating a tug of war. On one side are rising oil prices, risks to inflation expectations that the Bank of Canada (BoC) is sensitive to, and a Federal Reserve divided on the path forward. On the other are strong and accelerating corporate profits, growing investment tied to artificial intelligence (AI), a resilient consumer, and an economy that continues to defy fears of a slowdown. Understanding how these opposing forces interact helps explain not only where markets stand today, but how they may evolve in the months ahead.

Companies clear the bar during the busiest week of earnings season

Last week marked the peak of the first-quarter earnings season, with 181 S&P 500 and 41 TSX companies reporting results, including five of the Magnificent 7 (Alphabet, Amazon, Apple, Meta, Microsoft), placing a significant share of market leadership under the microscope at once. In aggregate, companies delivered, with results largely validating the view that corporate profits remain strong and continue to provide an important offset to geopolitical uncertainty.

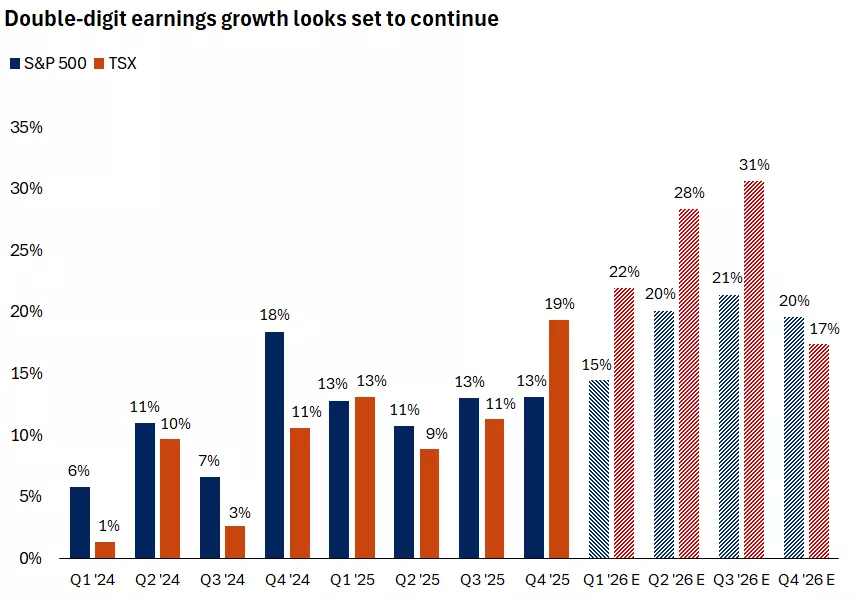

First‑quarter TSX earnings growth is now expected to exceed 20% and S&P 500 earnings is on track to grow 15%, which would mark the sixth consecutive quarter of double‑digit earnings growth. This strength has been driven by a combination of fast revenue growth and historically high profit margins. While the earnings season is still underway, we see several important themes that have already emerged.

The graph shows S&P 500 & S&P/TSX Composite earnings growth which has remained strong and is expected to accelerate in the quarters ahead.

The graph shows S&P 500 & S&P/TSX Composite earnings growth which has remained strong and is expected to accelerate in the quarters ahead.

- Strength is broad-based - Most sectors are participating, with U.S. technology, materials, financials, and industrials leading the way, all posting solid double‑digit growth. Health care and energy are the only two sectors where earnings are lower compared with a year ago, though declines are expected to reverse in the quarters ahead. Looking further out, all 11 sectors are expected to contribute to earnings growth in 2026, which is now projected to exceed 18% in the U.S. In Canada, growth may be even faster, with the TSX earnings estimated to rise 25% on the back of strength in energy and materials.

- Middle East tensions have not yet materially affected demand - Outside of airlines and other areas directly exposed to higher fuel costs, most companies report limited near‑term impact on demand from geopolitical uncertainty. While management teams continue to flag risks if tensions persist, few are seeing meaningful effects show up in orders and spending so far.

- The consumer remains resilient – Credit card companies continue to report healthy spending trends in the U.S. American Express, which skews toward higher‑income households, noted stable and strong activity. Visa reported no signs of weakening even among lower‑spending consumers, while Mastercard highlighted solid overall demand, despite some slowdown in overseas spending.

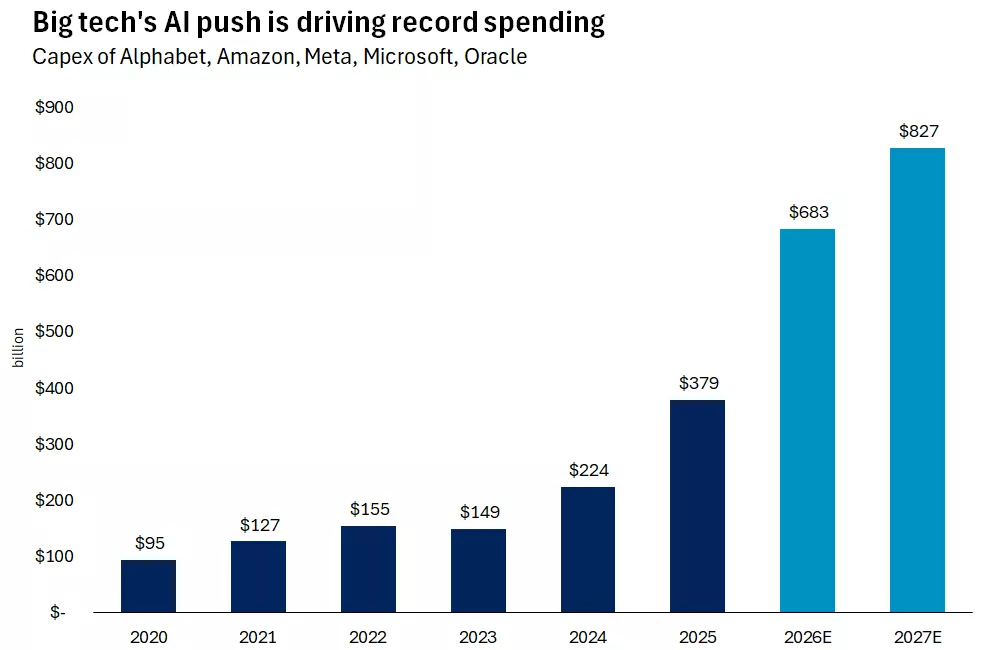

- AI remains a powerful driver – Accelerating AI adoption and spending continues to be the dominant force supporting earnings growth. Although stock reactions varied among the five mega-cap tech companies that reported last week, all exceeded earnings expectations. These results support the technology sector’s roughly 45% earnings growth outlook for the quarter, which has been revised sharply higher from about 26% just six months ago. Looking ahead, there is no sign of slowing on AI infrastructure spending. The large cloud firms (Amazon, Alphabet, Microsoft, Meta, and Oracle) are now collectively expected to invest roughly $700 billion this year to support AI‑related buildout, an increase of about 80% from a year ago. This spending may raise questions about investment returns, but should continue to support earnings for semiconductor companies and firms tied to data-center construction and equipment, in our view. In addition, we believe ultimately other sectors, like industrials, should benefit from the productivity gains from AI.

The graphs shows that the large cloud firms (Amazon, Alphabet, Microsoft, Meta, and Oracle) are now collectively expected to invest roughly $700 billion this year to support AI related buildout.

The graphs shows that the large cloud firms (Amazon, Alphabet, Microsoft, Meta, and Oracle) are now collectively expected to invest roughly $700 billion this year to support AI related buildout.

GDP confirms that the economy is holding up

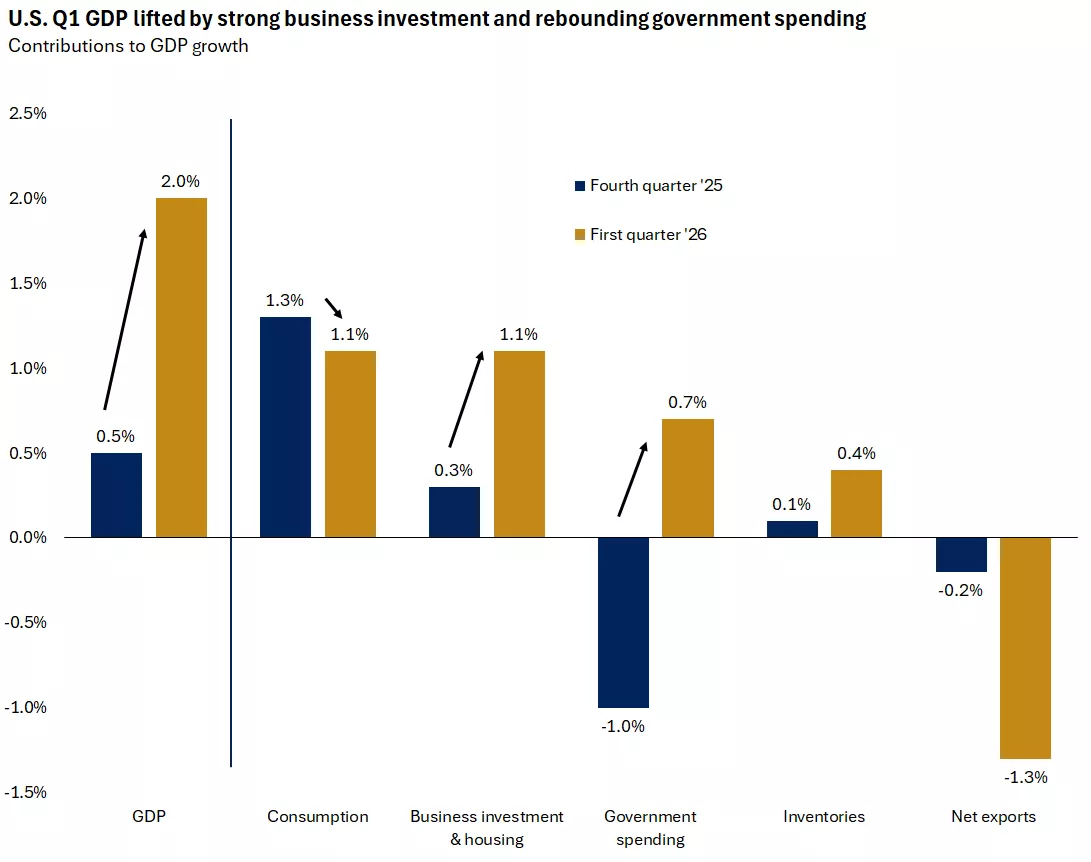

Recent economic data help reinforce what earnings have been telling us. Canada's GDP looks to have rebounded to 1.5% in the first quarter, in like with the BoC's projection. The U.S. economy also remains on solid footing. Real U.S. GDP grew at a 2% annualized pace in the first quarter, recovering from the drag caused by last year’s government shutdown.

Beyond the headline number, the details were even more favourable, with final sales to private domestic purchasers, a measure that strips out inventory swings, government spending, and trade effects, rising 2.5%, pointing to heathy private‑sector activity.

Consumer spending slowed modestly but remains resilient. Rising incomes and higher tax refunds helped offset higher gasoline costs. While energy prices may increasingly weigh on spending as refund season fades, there is no evidence yet of broad deterioration in consumer demand. Elsewhere, business investment was the clear standout. Spending on IT equipment and software alone added roughly 1.5% to GDP growth, reflecting continued AI investment.

Taken together, the data suggest that while higher oil prices may act as a headwind if they persist, there is currently little indication that the U.S. or Canadian economy are cracking.

The graph shows that the U.S. economy rebounded in the first quarter driven by strong business investment, a resilient consumer and higher government spending following last year's shutdown.

The graph shows that the U.S. economy rebounded in the first quarter driven by strong business investment, a resilient consumer and higher government spending following last year's shutdown.

The counterweights: Growing central bank uncertainty, energy, and rates

While earnings and economic data have been supportive, markets are not without meaningful counterweights. Rising energy prices, higher bond yields, a vigilant BoC, and a more divided Federal Reserve are injecting some uncertainty into the outlook.

The BoC held rates steady last week, as was widely expected. But while it continued to signal that it would look through any energy-driven uptick on inflation, it also acknowledged that near-term inflation expectations have moved up. South of the border, the Fed held policy steady for a third consecutive meeting, keeping the fed funds rate in the 3.5% - 3.75% range. While rates were unchanged, the tone of the decision leaned more cautious. A growing number of officials are less confident that the next policy move will be a rate cut, reflected in three dissents related to easing language in the statement. These dissents signal concern that inflation could remain elevated for longer.

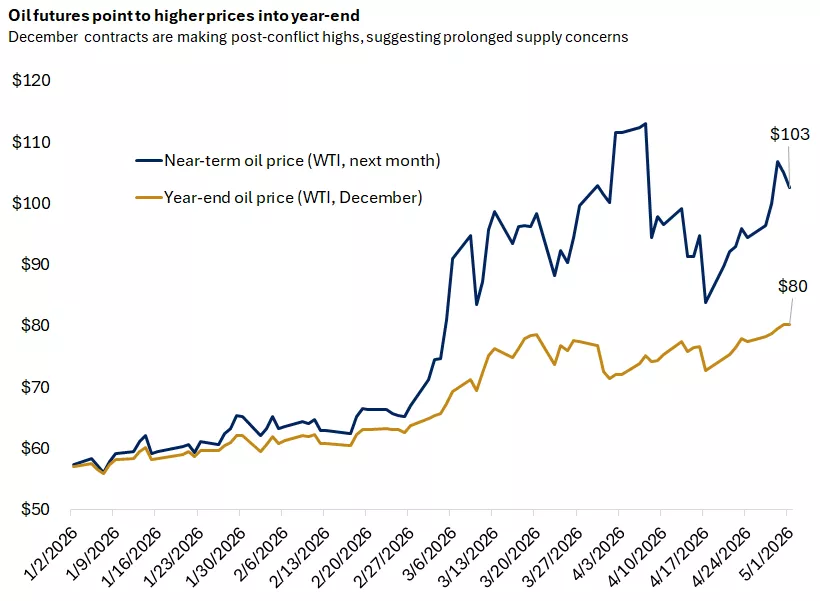

That concern is supported by recent inflation data. The Fed’s preferred measure, core PCE inflation, rose 3.2% in March, moving further away from the Fed’s 2% target. At the same time, energy markets are adding another layer of complexity. December oil futures have pushed to new post‑conflict highs, reaching $80, putting upward pressure on inflation expectations and bond yields.

Meanwhile, downside risks to the labour market appear to have eased, which is positive for the economy, but also reduces the urgency for policy easing. Initial jobless claims recently fell to 189,000, one of the lowest readings on record, and employment conditions remain supportive of consumer spending despite higher energy costs.

Taken together, these dynamics suggest to us that the BoC and the Fed are likely to remain firmly on hold in the near term, balancing solid economic momentum against inflation risks tied in part to energy prices. Even with the leadership change at the Fed, as Kevin Warsh will likely get confirmed to become the next chair in time for the June 16-17 meeting, we expect that the near‑term policy outlook would likely look similar, with inflation still elevated and labour‑market risks diminished. We still think one Fed rate cut is possible in 2026, but it may come at the very end of the year assuming energy markets have normalized by then. In Canada there is a possibility of rate hikes as the BoC policy is already at the low end of neutral, but we don't think the bank will make any move ahead of the summer CUSMA negotiations.

The graph shows that year end oil futures prices have begun to move higher, even as near term prices appear to have peaked.

The graph shows that year end oil futures prices have begun to move higher, even as near term prices appear to have peaked.

Bottom line: Earnings remain a reliable anchor

Markets have come a long way over the past month, and the path forward is not without obstacles. Though the situation remains fluid with Iran submitting a fresh peace proposal, there is no clear resolution in sight for the ongoing energy supply disruptions, and central banks remain on hold with a slightly more hawkish tilt. Against that backdrop, it is not surprising to us that stocks and bonds are responding to different narratives. Equity markets have leaned into a technology‑led rally in the U.S. and a commodity-led rally in Canada supported by strong earnings, while bond markets have focused more on the risks from higher oil prices, inflation, and policy uncertainty.

After such a strong advance, upside and downside risks now appear more balanced, and we think a pause in the stock rally would be a reasonable expectation. Even so, the earnings backdrop provides an important cushion, in our view. As long as corporate profits continue to accelerate, we think investors have good reason to avoid getting overly negative and to tune out, rather than react to, the daily headline noise.

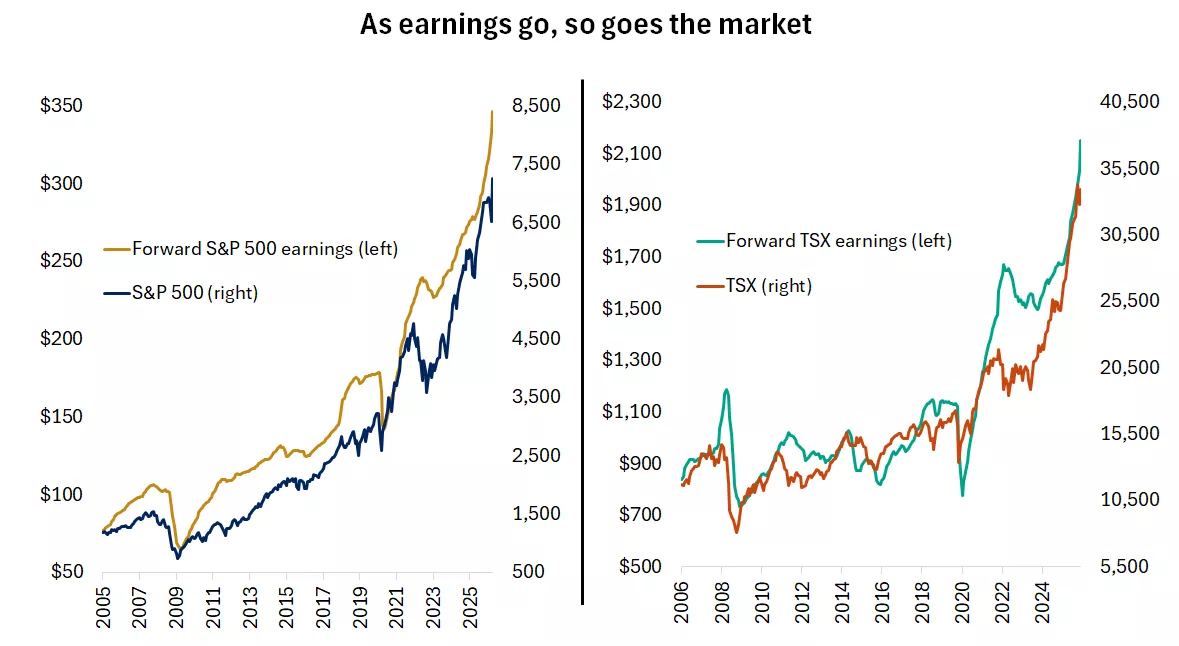

For now, earnings appear to be winning the tug of war. As earnings go, so goes the market, and corporate profits remain one of the market’s most reliable anchors.

The graph shows that over the long-term there is a strong relationship between stocks prices and corporate profits.

The graph shows that over the long-term there is a strong relationship between stocks prices and corporate profits.

Angelo Kourkafas, CFA

Senior Global Investment Strategist

Sources for all data in commentary: Bloomberg, FactSet

The Week Ahead

Important economic events and data for the week ahead include the domestic and U.S. payrolls report for April and the ISM services PMI.

Previous weeks' weekly market wraps

Angelo Kourkafas

Angelo Kourkafas is responsible for analyzing market conditions, assessing economic trends and developing portfolio strategies and recommendations that help investors work toward their long-term financial goals.

He is a contributor to Edward Jones Market Insights and has been featured in The Wall Street Journal, CNBC, FORTUNE magazine, Marketwatch, U.S. News & World Report, The Observer and the Financial Post.

Angelo graduated magna cum laude with a bachelor’s degree in business administration from Athens University of Economics and Business in Greece and received an MBA with concentrations in finance and investments from Minnesota State University.

Important information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved of owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent to international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.